His tax returns show a blank where the Social Security line should be. What that empty line teaches about when to claim is worth more than the check he is skipping.

We just pulled up Joe Biden’s Social Security check and unpacked the tax trap hidden inside it. Donald Trump’s tax return is the mirror image, and it lands on a fitting week.

This Sunday, June 14, the president turns 80. It is also Flag Day, which feels about right for a man who has never been shy about the symbolism. And it makes this a perfect moment to ask the exact question the Biden piece raised, only pointed in the other direction: how big is Donald Trump’s Social Security check?

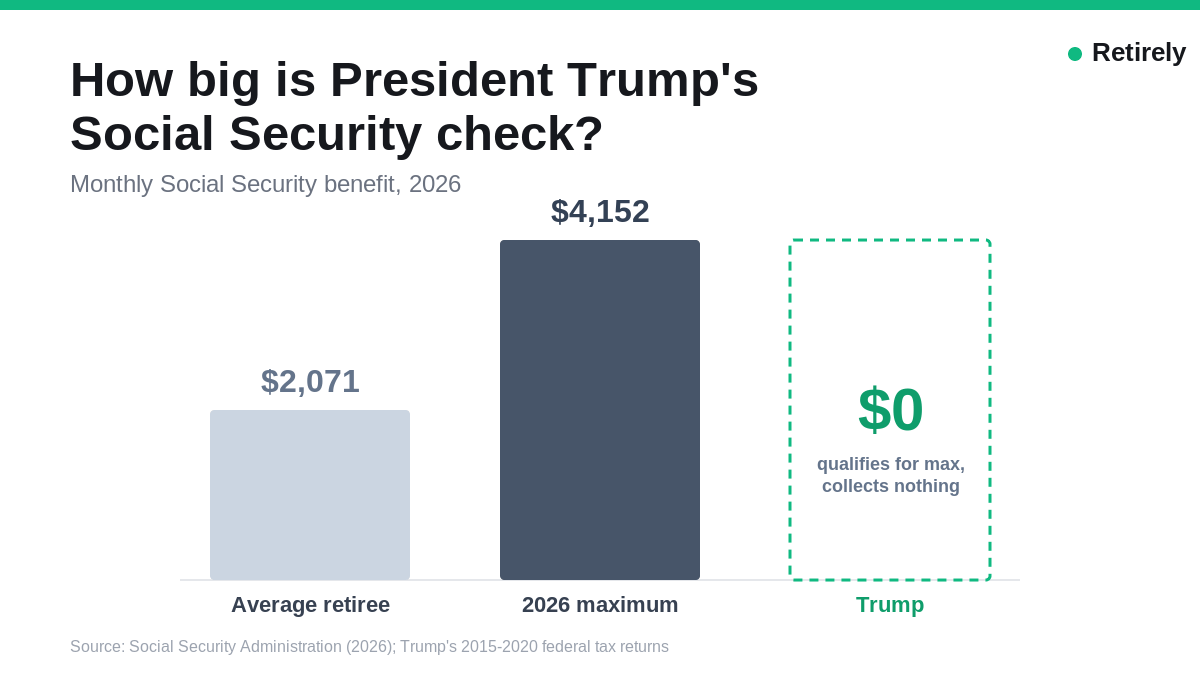

The answer, down to the dollar, is zero.

When the House Ways and Means Committee released Trump’s tax returns covering 2015 through 2020, the most recent ones the public has ever seen, the line for Social Security income was left blank. Every single year. At 79, soon to be 80, Trump long ago earned his 40 credits, sailed past his full retirement age, and almost certainly qualifies for something near the largest benefit the program pays out. He simply never filed the paperwork to collect it.

Put that reality next to the rest of us. The absolute most a worker retiring at full retirement age can claim in 2026 is $4,152 a month, and waiting until age 70 pushes that number past $5,000. Meanwhile, the average retired worker collects about $2,071. Trump qualifies for the very top of that scale and draws none of it, while Joe Biden, who is three years older into retirement, banks roughly $3,570 a month. One former president takes close to the most the system allows. The current one takes nothing.

Why would anyone willingly walk away from a maximum government check? Because they can afford to. “It’s not necessarily uncommon that the real high earners just skip Social Security,” Jim Blair, a former Social Security administrator, noted when Trump’s blank line first made news. Wealthy filers qualify exactly like everyone else, because the program is not means-tested. You paid into the system, so you are owed the benefit, no matter how many golf courses or skyscrapers you own.

Whether the wealthy should claim is the kind of argument that fills up internet comment sections, and reasonable people land on both sides of the fence. Andrew Biggs, a former Social Security official now at the American Enterprise Institute, put one side of the argument plainly: “Not only did you pay for the benefit, you were forced to pay for the benefit. I don’t think anyone can question if you decide to accept it.” In nearly the same breath, he allowed that whether the system should be sending checks to billionaires at all is an entirely fair thing to question. Both things can be true at once.

But the theoretical debate about billionaires and government benefits is a distraction from the mathematical reality. Here is the part that actually matters for your own check, buried under the famous blank line on that tax return.

Trump is not being shrewd by waiting. He is actively losing money. Social Security rewards patience, but only up to a very specific, unforgiving point. For every single year you delay claiming past your full retirement age, your benefit grows by about 8 percent. That is a guaranteed, government-backed raise that is almost impossible to match safely anywhere else in the financial world. It is the primary reason financial planners beg their clients to hold off claiming if they have the cash reserves to do so.

But that 8 percent bonus stops cold the exact day you turn 70. There is absolutely no credit for waiting a single day longer.

Trump is now a full decade past that finish line. That means every single month he does not claim is a month of a maximum benefit gone for good. When you file past age 70, the government will pay at most six months of benefits retroactively. The rest of those missed checks simply evaporate into the bureaucratic ether. At a maximum benefit of over $4,000 a month, walking away from a decade of payments means leaving roughly half a million dollars sitting in the Treasury. That is a massive sum of money that could have been reinvested, given to heirs, or donated to charity.

So while the flashy headline is that a billionaire skips his monthly check, the most useful lesson is the exact opposite of what his example suggests. If you are nearing the finish line, there are three things absolutely worth doing to ensure you do not accidentally mimic the Trump strategy.

First, if you can afford to wait, you should wait, but never past age 70. Delaying your claim from age 67 to 70 can lift your monthly benefit by roughly a quarter. Delaying past 70 lifts it by nothing at all. Claim the exact day you turn 70 at the latest. If you are already past 70 and have not filed the paperwork because you are still working or simply forgot, fix that this month. You are leaving free money on the table, and the government is not going to call to remind you.

Second, look at who else might be standing on your earnings record. Social Security is not just an individual retirement account; it is a family insurance policy. A spouse can draw a benefit based on your earnings, worth up to half of your full retirement amount. Even more critically, survivors can draw on it after you are gone. When one spouse passes away, the surviving spouse steps into the larger of the two household checks. If you maximize your benefit by waiting until 70, you are permanently maximizing the survivor benefit you leave behind for your widow or widower. If you die first, that larger check continues to support them for the rest of their life. Your claiming decision is rarely just about your own lifespan. It is about the financial safety net you leave behind. This is one more reason Trump’s blank line is not the model to copy for the average family.

Third, weigh the taxes before you assume a bigger check is a pure windfall. As we saw with the Biden analysis, if you have other income, up to 85 percent of your Social Security benefit becomes taxable once your combined income clears $25,000 as a single filer or $32,000 as a married couple. Those thresholds have not moved an inch since they were written into law in the 1980s. Every year, ordinary inflation pushes more middle-class retirees over the line.

For someone in Trump’s massive tax bracket, a heavily taxed benefit is part of why skipping it entirely is not quite as strange as it sounds. When you factor in top-tier federal and state income taxes, the net value of that check shrinks significantly. Furthermore, high earners are subject to Medicare premium surcharges known as IRMAA, which are directly tied to tax returns. For most ordinary retirees, however, crossing the tax threshold just means you need to plan around the tax bill by having taxes withheld directly from the check, instead of being ambushed by the IRS in April.

Donald Trump can leave a maximum check on the table for a decade and never feel a single pinch. He can afford to fund his own lifestyle without relying on the exact system he paid into for fifty years. That is the luxury of his unique financial situation, not a blueprint for yours.

The rest of us should do the unglamorous, mathematically sound thing: claim by 70, mind the spousal and survivor benefits, and take every single dollar we were, in Biggs’s words, forced to pay for.

Happy 80th, Mr. President. The check is there whenever you want it.

5 Comments

Isn’t a person penalized financially if that person fails to take his/her Social Security at the age of 70?

There is not “charge” to you as a penalty. There is only the loss of money you could have received if you do not file by the month of the last increase. By filing on the month or your last possible increase, every month your earned benefit (before deductions) will be the most it will ever be and it is not reduced as it would be if you filed earler than that final month of waiting. I have maxed out paying into SS for more years than is needed to get a max when I filed at (I think) age 70-1/2. Whether that age is still the earliest to get the max monthly is not likely, since they seem to raise it offen. At any rate, I am now more than 10 years past that age and my monthly earned from SS is $5,023.90 before deductions. People who have not annually maxed out on SS payroll deductions due to high salaries will of course get less.

That maximum is not true. Even after deductions my net check deposited is more than that. My full benefit for 2026 before deductions is $5,023.90 per month

Your benefit must include Delayed Retirement Credits and also Cost of Living increase for 2026.

There is a LEGAL MAXIMUM monthly benefit that can be paid.

There is an additional wrinkle. There are limits to the amount of healthcare the federal Medicare will pay. If you want to receive healthcare beyond that it is not only on your own dime, but you have to disenroll from Medicare AND Social Security and pay back the Social Security you have already received. Thank you, Bill Clinton.