Joe Biden is one of the few Americans whose exact benefit is public record. The real story is not the number. It is the tax trap hiding inside your own check.

Hunter Biden is back online and impossible to ignore. His 83-year-old father collects a Social Security check the rest of us can actually see, and its size carries a warning.

The prediction markets have already opened a line on whether Hunter Biden runs for president in 2028, which tells you everything about the week he is having.

After years as the internet’s favorite punching bag, the former president’s son reappeared on X in late May and has not logged off since. He has picked up more than 400,000 followers in a matter of days, traded jabs with his old critics, marked seven years sober in a June 1 post, and earned a nickname even some of his detractors seem to enjoy: the MAGA whisperer. President Trump, asked about him in the Oval Office, allowed that Hunter could “possibly” win in 2028. Agree with the man or not, he is the most talked-about Biden in the country right now.

Which makes this a good moment to look at the quietest one.

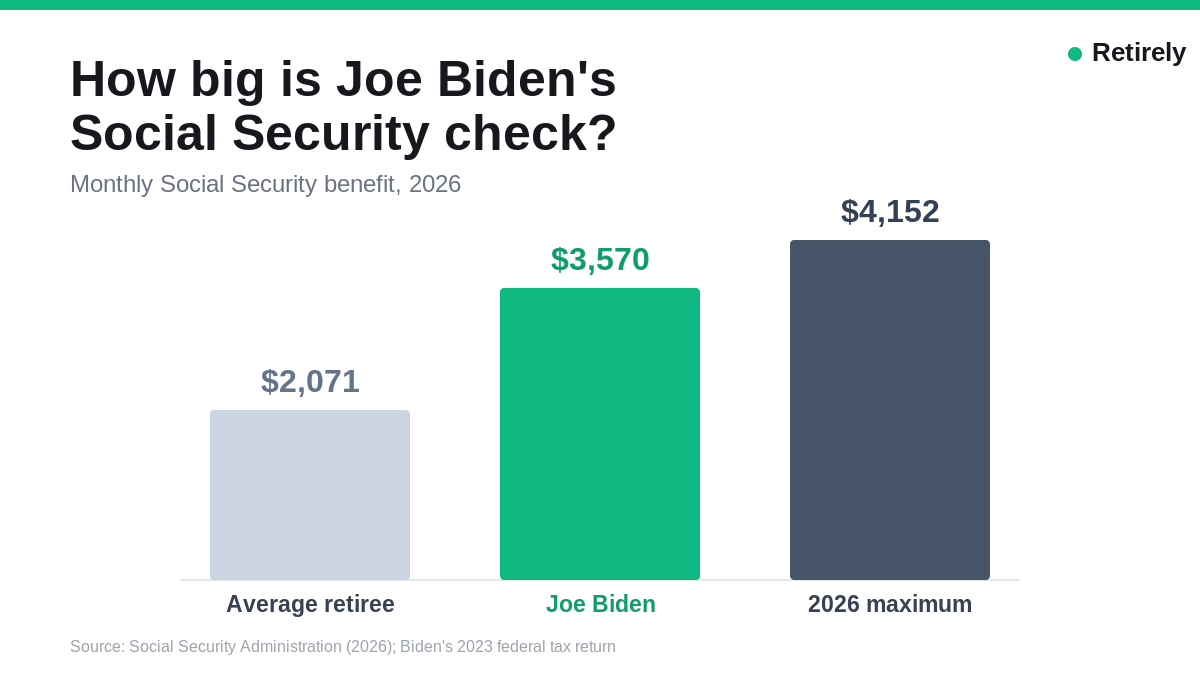

While Hunter trends, his father sits on a piece of public information almost no other retiree’s family has. Because Joe Biden released his tax returns for years, we know, close to the dollar, how big his Social Security check is. On the 2023 federal return he made public, the most recent one available, Biden reported $42,842 in Social Security benefits for the year. That is about $3,570 a month. Add his wife Jill’s benefits and the household collected $64,254, or roughly $5,355 a month, on an adjusted gross income of just under $620,000.

Now set that next to your own. The average retired worker in 2026 collects about $2,071 a month after this year’s 2.8 percent cost-of-living raise. Biden’s personal check is nearly three-quarters larger. And yet here is the first thing the famous number teaches: it is not unlimited. The most any worker retiring at full retirement age can claim in 2026 is $4,152 a month. Biden, a man who has reported more than $11 million of income in a single year, draws a check that still sits below that ceiling.

That is the part most people get wrong about Social Security. The benefit formula stops counting income past an annual cap, which sits at $184,500 in 2026. Earn $200,000 a year or $11 million, and above that line the program treats you exactly the same. A former president and a retired plant manager who both maxed out their careers land at the exact same ceiling. Social Security was built to replace a slice of a working wage, not to scale with wealth, and Biden’s check is a clean illustration of the cap doing its job.

Here is what nobody writes about, though, buried under the famous name.

Biden does not just collect Social Security. He pays tax on it. About $54,616 of the family’s benefits, roughly 85 percent, was subject to federal income tax. For a couple pulling in $620,000, that sounds fair enough. The trouble is that the rule taxing him is the exact same rule quietly taxing your neighbor on a $2,000 check.

Social Security benefits become taxable once your combined income crosses $25,000 for a single filer or $32,000 for a married couple. Those numbers were written into law in 1983, with a second tier added in 1993, and Congress has never once adjusted them for inflation. A $25,000 line drawn in 1983 would be worth more than triple that in today’s dollars if it had kept pace with inflation. It did not move at all. So every year, ordinary cost-of-living raises and modest pensions nudge more middle-income retirees across a threshold that has stood completely frozen for four decades. Biden crosses it because he is wealthy. Millions of ordinary retirees cross it simply because the line never followed the value of a dollar.

The good news is that this is one of the few taxes you can actually plan around. Three strategic moves matter most.

First, know your true number. Combined income is your adjusted gross income, plus any nontaxable interest, plus exactly half of your Social Security benefit. If that total is anywhere near $25,000 on your own or $32,000 as a couple, you are officially in the taxable zone. It is highly worth running the math before December, not after.

Second, actively manage the income that crosses the line. Converting a portion of assets to a Roth IRA in a low-income year, sending required IRA withdrawals straight to charity through a qualified charitable distribution (which never lands in your AGI), and spacing out large investment withdrawals instead of taking them all at once can each keep more of your benefit out of the taxable column.

Third, decide exactly how you will pay. You can ask the Social Security Administration to withhold 7, 10, 12, or 22 percent of each check so a surprise tax bill does not ambush your cash flow in the spring. And if you have not claimed your benefit yet, remember the lever that does the most heavy lifting of all: waiting until age 70 pushes the maximum benefit higher still, past $5,000 a month in 2026. That is the closest any regular earner gets to a presidential-sized check.

Biden, for his part, used one of his few public appearances since leaving office to defend the program, warning last year against cuts to it. That political fight will easily outlast this news cycle, and the next one.

The prediction markets can keep arguing about whether a Biden will be on a ballot in 2028. The more useful bet is the one you can actually win this year, and it has absolutely nothing to do with anyone’s last name: learn where the $25,000 line sits before it learns where you are. Hunter got the headlines. The financial lesson belongs to the rest of us.

4 Comments

In the article, you write that “For a couple pulling in $620,000, that sounds fair enough. The trouble is that the rule taxing him is the exact same rule quietly taxing your neighbor on a $2,000 check.” That is true if you mean that 85% of his SS is taxed just like anyone else’s SS. However, the rate of that tax could be lower for anyone else if their adjusted gross income was lower, right?

This criminal should be in prison and not receiving a check!! His regime to go with!!

It simply establishes the fact that us regular citizens don’t have a chance in hell to be treated like we should be.

It’s a crime to be treated like a worthless citizen!!!

EVERYONE knows his REAL nickname is “Humper.” Duhhhhhhhh