Got a decent amount of money right now that you’d like to turn into a seven-figure stash by the time you retire? Well, good news… it’s probably possible. The key to doing so is just a combination of how much time you’ve got and what you do with that money in the meantime. If you’ve got enough of both, it’s possible for you to turn $100,000 into $1 million. Here are a few ways you can make it happen.

1. Own quality growth stocks for 25 to 30 years

Many new investors start their journeys by buying some of the market’s most popular growth stocks. And understandably so. These tickers (by definition) are expected to continue growing in value.

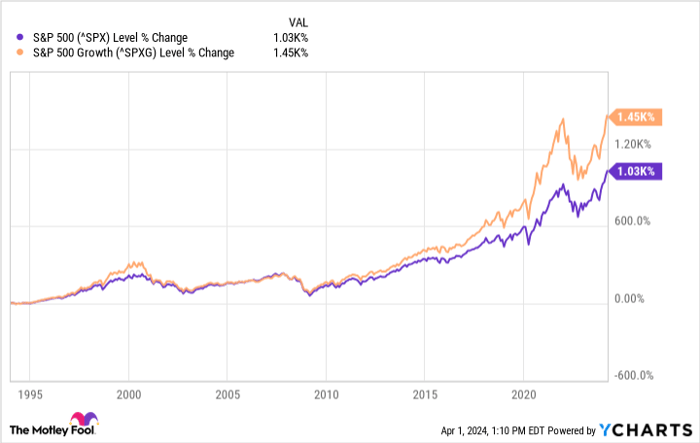

They’ve also got a collective track record to justify this interest. Over the course of the past 30 years the S&P 500 Growth index has outgrown the S&P 500 (SNPINDEX: ^GSPC) by nearly half as much more than the market’s most-used benchmark gained during that period.

Sticking with growth stocks for the entirety of this span wouldn’t have been easy for investors, however.

See, while the S&P 500 feels volatile, it’s not nearly as volatile as the S&P 500 Growth Index and its underlying stocks are. They’re so volatile, in fact, that at times it would have been tough to stick with many of these names. And if you can’t stay in stocks when things get ugly, you risk missing out on most of their upside. That’s because stocks’ biggest gains often come immediately after their biggest sell-offs, and right at the very beginning of new bull markets… when many investors still don’t believe the bear market is over, and are therefore on the sidelines. Big mistake.

2. Reinvest the dividends of proven dividend-paying stocks

Growth stocks aren’t the only way of producing big investment gains, however. Boring old dividend stocks can do the same.

This may seem counterintuitive on the surface. Dividend stocks tend to be shares of slower-moving, lower-growth companies, after all.

But, don’t dismiss the upside of slow and steady value-creation in the form of cash — particularly when the companies in question are in the proven habit of raising their dividend payouts. These quality stocks ultimately tend to outperform their non-dividend-paying peers. Mutual fund company Hartford did some data-mining on the matter, determining that in the 40-year span from 1973 to 2023, the more willing and able a company was to pay a dividend, the better its stock performed. These stocks also tend to be less volatile (lower beta), making them even easier to hang onto when things become turbulent for the market.

| Dividend Profile | Average Annual Returns | Beta |

|---|---|---|

| Dividend growers/initiators | 10.2% | 0.89 |

| Dividend payers | 9.2% | 0.94 |

| No change in dividends | 6.7% | 1.02 |

| Dividend cutters/eliminators | (0.6%) | 1.22 |

| Dividend non-payers | 4.3% | 1.18 |

| Equal-weight S&P 500 index | 7.7% | 1.00 |

Data source: Hartford Funds and Ned Davis Research

For reference, reinvesting the dividends paid by the highest-quality dividend stocks returning (net) on the order of an average of 9% to 10% per year would grow $100,000 into $1 million in roughly 25 years, a result that’s in line with growth stocks’ historic long-term returns.

The only catch is, you really do have to reinvest those dividends into more shares of those dividend-paying names to produce these kinds of results. Hartford adds that over the past several decades, dividends accounted for around one-third of the S&P 500’s net gains, and since 1960, reinvested dividends drove about 85% of the index’s cumulative returns. Just know that most of these net gains will come closer to the end of any time frame than to the beginning of it.

3. Own “the market” via an index fund for two or three decades

But what if you think a dividend-oriented strategy is too far to the other extreme? There’s a hybrid approach that’s both simpler and zero-maintenance. Why not just own the market as a whole through an index-based instrument like the SPDR S&P 500 ETF Trust (NYSEMKT: SPY), which merely mirrors the S&P 500’s performance (for better and for worse)?

Boring? Sure… a little. This approach, however, avoids many of the inherent problems of being an investor these days.

Chief among these sidestepped problems is that if you buy and hold an index fund, you don’t experience the risky temptation of trying to perfectly time a trade’s entry or exit. The idea is to simply plug you into the overall market’s long-term performance, which is an average gain of about 10% per year.

Yes, some years are better while others are worse. In that you know you can’t know when these near-term ebbs and flows are going to take shape though, you don’t even bother trying. You simply let time work its magic over the course of two to three decades, smoothing out all the market’s highs and lows that surface in the interim en route to growing $100,000 into $1 million.

Another upside: This strategy also allows you to avoid making constant check-ins on your stocks or the market’s current condition. Such check-ins often spur impromptu buying and selling you may not really want to do, but feel like you have to at the time just because you’re already looking.

4. Try a combo approach, but mostly, take the bigger hint

There’s a fourth option, of course. That is, utilize all three strategies. Start with a foundational index fund, then add dividend stocks (don’t forget to turn on the DRIPs), and then pick up some growth stocks you have good reason to believe will still be thriving 10, 20, and even 30 years down the road. This approach provides you with balanced exposure to the key upsides of all three strategies. You’ll also find that this blended approach leaves your entire portfolio’s value relatively steady from one month and even one year to the next.

Just notice the common thread in all three strategies. That’s time — in all three scenarios above, the path to turning a small six-figure sum into a $1 million retirement nest egg took 25 to 30 years, depending on the market environment at the beginning and then at the end of the time frame. Giving yourself enough time to achieve the goal is far more important than whatever stock-picking strategy you use. Conversely, not giving yourself enough time to meet your investment goal is the biggest investment risk you can take.

A close-second risk: Not doing anything constructive with your money once you’ve worked so hard to save up a meaningful amount of it to put to work for your future.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

View the “Social Security secrets”

James Brumley has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.