How soon do you want to retire? For most people, the answer to the question is “as soon as possible.” For too many people, though, “as soon as possible” is further away than they like. There’s just not enough money saved up, and Social Security isn’t going to cut it if you start your retirement benefits at the earliest possible age of 62.

The good news is that nearly anyone can retire a little bit earlier than you might believe possible. The bad news is that one silly mistake is preventing that from happening. That simple, avoidable mistake is waiting too long to get serious about building your retirement nest egg.

Image source: Getty Images.

Starting earlier does more good than investing more later

If you’re putting off getting started, you’re not alone. It’s easy to get discouraged before you even start, so much so that you never even bother starting. That’s particularly true in your early working years when you’re not earning as much as you will later in life. Then, by the time you start making decent money and have some discretionary funds left over at the end of the month, it feels like it’s too late to matter. Talk about a catch-22!

Both excuses, however, are rooted in errant assumptions. The truth is, it’s rarely too late to get started, and it doesn’t take a ton of money to get a meaningful start on your retirement fund.

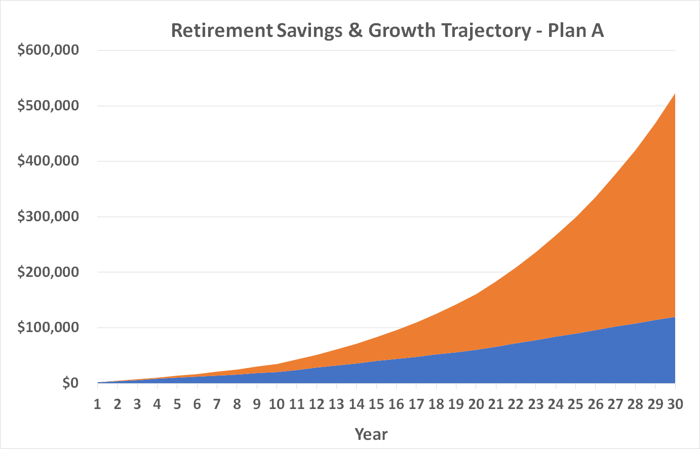

To illustrate the point, we’ll use a simple but highly applicable hypothetical scenario — let’s call it Plan A. Plan A assumes that for the first 10 years of a 30-year career, you can only tuck away $2,000 per year, but during the second 10-year stretch of a 30-year career you’re earning better money and can come up with an extra $4,000 per year to invest in an S&P 500 (SNPINDEX: ^GSPC) index fund averaging an annual return on the order of 10%. Then, in the last 10 years of your 30-year career, you’re earning even better money and can put $6,000 to work every year in the same fund. How much do you think you might have at the end of that period? Try a whopping $523,000!

Data source: Calculator.net. Image by author.

The key here is compounding, or earning returns on your previous growth. Your annual contributions are driving more growth than net investment gains are through the first seven years of the 30-year span. Beginning in the eighth year of saving, though, the returns on your gains and contributions start to dramatically exceed your yearly contributions. They never look back, either.

And the cost of waiting? Huge.

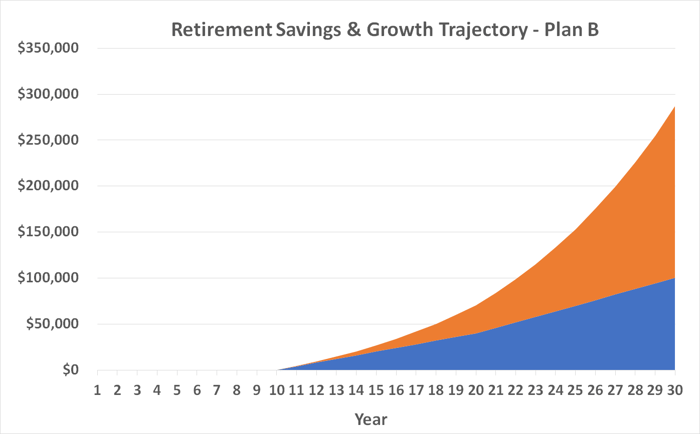

Just to drive the point home, let’s not make the annual $2,000 contribution to the retirement fund for the first 10 years of the 30 years in question, yet leave everything else the same; we’ll call this Plan B. Just by skipping that seemingly modest period of investment, what would have been a portfolio worth more than half a million dollars is instead only worth $287,000 — a little more than half the amount grown in the first scenario.

Data source: Calculator.net. Image by author.

Connect the dots. Even the smallest of starts means so much more, given the amount of time it was allowed to grow, and then grow some more, and then grow some more after that.

Oh, and in case you were wondering, if you didn’t save at all for the last 10 years of the 30-year span but still invested as described above for the first 20 years of the three decades in question — call it Plan C — you’d still end up with over $417,000 as the end of your 30-year career.

Data source: Calculator.net. Image by author.

As was said, time is the key.

Anything is better than nothing

But you can’t come up with $2,000 per year to put into a retirement account? Or, maybe you don’t have 30 years until you have to retire? It doesn’t matter. The example above was just an exercise, even if it is relatable to most people. If you can do more, do more. If you have to start with less, then start with less.

The point is to simply start somewhere, even if it feels like the start is too small to matter. It isn’t. Time does the bulk of the heavy lifting when it comes to building a retirement fund. It does the same amount of heavy lifting, however, no matter how much or how little you put to work. Just get started.

10 stocks we like better than Walmart

When our analyst team has an investing tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and Walmart wasn’t one of them! That’s right — they think these 10 stocks are even better buys.

Stock Advisor returns as of July 17, 2023

James Brumley has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.