In 2026 the breaks got bigger than they have been in decades. The applications are still the part nobody mentions.

Polymarket will let you bet on almost anything. You can put real money on the next Fed cut, the box office for a movie that is not out yet, or whether it snows in Times Square on New Year’s Eve. What the platform does not have is a market for whether a 71-year-old retired nurse in Toledo files the one-page form that would knock a few hundred dollars off her property tax bill this year. There is no line for that. No live odds, no trading volume, no cheering crowd on financial Twitter. And yet that quiet little piece of municipal paperwork is one of the surest money moves available to an American retiree right now, which is exactly why almost nobody is talking about it.

Start with what just happened, because 2026 turned out to be a banner year for senior property tax relief and it arrived with almost no fanfare. In November, Texas voters approved a measure that raised the extra school-tax exemption for homeowners 65 and older from $10,000 to $60,000. That sits on top of the new $140,000 general homestead exemption, so a Texas senior now shields $200,000 of value from school taxes and freezes the school portion of the bill besides. In New York, a law signed in December lets localities lift the senior exemption from half a home’s assessed value to as much as 65 percent. That is the first increase of its kind in decades, and it is worth around $300 a year to the average qualifying owner. In New Jersey, the most expensive property tax state in the country, the new Stay NJ program mailed its first checks in February 2026, reimbursing eligible seniors for half their bill up to $6,500.

Ohio, Montana, Florida, and Wyoming all moved on senior or homeowner relief in the same stretch. If you only read the headlines, you would think nothing happened. Property taxes are not a sexy beat. They do not trend. They just quietly, ruthlessly decide whether a retired teacher can afford to stay in the house she raised her kids in. It is a slow squeeze, and the relief valves are hidden in plain sight.

Here is what nobody is writing about. This is not a handful of unusually generous states. It is nearly all of them. We pulled together every state’s senior property tax programs into one map, and the pattern is striking. From Alabama to Wyoming, almost every state offers people over 65 some combination of an exemption that shrinks your taxable value, a freeze that stops it from climbing, a credit that pays you back directly, or a deferral that lets you postpone the bill entirely until the home is sold.

Alaska exempts the first $150,000 of value outright. South Carolina takes the first $50,000 of market value off the bill entirely. Colorado knocks out half the value of the first $200,000 if you have lived there for a decade. The deeper levers are stranger still. California lets homeowners carry their tax base with them from age 55, so downsizing does not trigger a tax spike. Pennsylvania’s rebate of up to $1,000 kicks in at 65, and opens to widowed residents as early as 50. Massachusetts offers a potent cocktail of exemptions, deferrals, and a circuit-breaker credit, with qualifying ages running from 65 to 70 depending on the program. The mechanisms differ wildly, and the dollar amounts range from a nice dinner out to a life-changing sum, but the door exists almost everywhere.

And almost nowhere does the door open by itself. This is the catch that costs retirees real money: with very few exceptions, none of this relief is automatic. The county does not look up your birthday and apply the discount. You have to know the program exists, confirm you qualify, and file. The Texas Comptroller says it plainly: a property owner must apply for the exemption. New York makes you file Form RP-467 and, for many seniors, renew it. Miss the deadline, which can fall as early as February or March, and you wait a full year to try again, paying the full bill in the meantime.

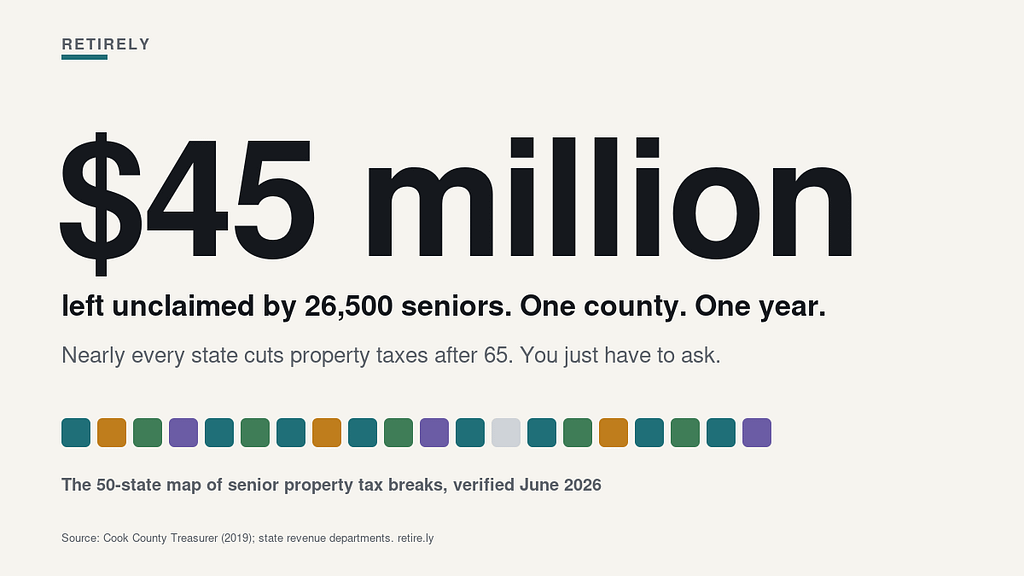

How much does the not-asking cost? The cleanest count comes from Cook County, Illinois, where the Treasurer’s office went looking. In 2019, the office estimated that 26,500 senior homeowners were leaving as much as $45 million on the table in a single year. Nearly all of them had received the same exemptions the year before. The relief required reapplying every single year, and people simply did not know, forgot, or gave up. The number was big enough, and embarrassing enough, that Illinois changed the law that August to make the basic senior exemption renew automatically. But the more valuable Senior Freeze still has to be filed manually every single year, and every year a fresh wave of seniors forgets to send it in. Cook County is not unusual in this regard. It is just one of the very few places that bothered to add up the unclaimed money out loud.

The forms themselves do not help. County tax websites are mazes of legal jargon, and for a 75-year-old navigating an assessor’s portal that looks coded in the dial-up era, the friction alone is enough to leave the money with the state.

So if you are 65 or older, or you are helping a parent who is, here is the part worth acting on.

First, look up your own state and assume you qualify for something until proven otherwise. The odds are with you. Start at your county assessor’s website, not a national lookup tool, because the real money is often in the local add-ons that vary from one town to the next.

Second, ask the assessor one specific question: which programs do I have to renew, and when is each deadline. The exemptions that auto-renew are not the problem. The freezes, deferrals, and income-based credits that require annual paperwork are where the money quietly leaks. Put those dates on a calendar the way you would a medication refill.

Third, if you are within ten or fifteen percent of an income limit, apply anyway. Make them tell you no. Many states use sliding scales rather than hard cutoffs, and several define income in ways that leave out Social Security or deduct medical costs. The number on the brochure is often not the number that applies to you.

Finally, do not assume your mortgage servicer is handling this. If your taxes are paid through an escrow account, the bank just pays whatever bill the county sends. It has no incentive to audit your age or hunt down exemptions; it simply raises your monthly escrow to cover the rising bill. Securing the exemption is on you, and once you do, the county bills the bank less and your monthly payment drops.

None of this will ever trend. There will be no Polymarket pool on whether your neighbor files her homestead paperwork before the March deadline, no live odds on the retired machinist in Ohio who does not realize his state just nudged the senior exemption up again. The biggest financial event in a lot of older homeowners’ year is a bland government form that takes twenty minutes and a photocopy of last year’s tax return, and it closes with a smaller number on next year’s bill that nobody live-streams and nobody celebrates.

That is, in its own quiet way, news. Good news, even. Just no one is taking bets on it.

The 50-state table

Compiled and verified against state revenue departments and official sources, June 2026. Programs change; confirm details with your county assessor before relying on them. Full sourced version: the Retirely data v2 VERIFIED sheet.

| State | Senior relief type(s) | Age | Income test? | Notes |

|---|---|---|---|---|

| Alabama | Exemption (state portion exempt at 65; full county relief with income test) | 65 | For full relief | State portion fully exempt at 65; full exemption needs federal taxable income $12K or less |

| Alaska | Exemption (first $150K mandated statewide) | 65 | No | AS 29.45.030(e); boroughs may exempt more |

| Arizona | Assessment freeze + state credit | 65 | Yes | Freeze renewable every 3 yrs; 2026 income $47712 single / $59640 multi |

| Arkansas | Assessment freeze + homestead credit | 65 | No | Amendment 79 freeze at 65; credit rises to $600 with 2026 bills |

| California | Tax-base transfer (55+) + deferral (62+) | 55/62 | Deferral: yes | Prop 19 portability; postponement income cap ~$55K + 40% equity |

| Colorado | Exemption (50% of first $200K) | 65 | No | 10 consecutive years ownership AND occupancy; portability on Nov 2026 ballot |

| Connecticut | Circuit-breaker credit | 65 | Yes | Up to $1000 single / $1250 married; towns may add more |

| Delaware | School tax credit + county exemptions | 65 | Varies | State credit 50% of school tax up to $500; 10-yr residency if domiciled after 2017 |

| DC | Senior deduction (50% tax reduction) | 65 | Yes | Income cap ~$160K (2025; adjusted annually); must own 50%+ of property |

| Florida | Local-option senior exemptions + assessment cap | 65 | Senior add-ons: yes | Save Our Homes 3% cap; local $50K senior exemption; full exemption for 25-yr residents on homes under $250K where adopted |

| Georgia | School-tax exemptions (county by county) | 62-65 | Varies | Statewide senior exemptions income-tested; many counties exempt school tax fully |

| Hawaii | Larger county home exemption by age tier | 60-70 (by county) | No | Honolulu $160K at 65 ($180K from 2027); Kauai $240K at 60 / $260K at 70 |

| Idaho | Circuit-breaker reduction | 65 | Yes | Up to $1500 off home + 1 acre; 2026 income limit $39130 after medical |

| Illinois | Exemption (auto-renews in Cook) + Senior Freeze (annual filing) | 65 | Freeze: yes | Freeze income cap $75K for 2026 then $77K/$79K (PA 104-0452) |

| Indiana | Over-65 credit ($150) + over-65 cap on bill increases (2%/yr) | 65 | Yes | SEA 1-2025 replaced the old deduction; income $60K single / $70K joint |

| Iowa | Senior homestead exemption ($6500 taxable value) + means-tested credit | 65 | Credit: yes | Exemption has no income test and auto-renews |

| Kansas | Refund programs (SAFESR 75% + homestead + SVR freeze refund) | 65 | Yes | SAFESR: income $25380 or less and home value $350K or less |

| Kentucky | Exemption (constitutional; indexed) | 65 | No | $49100 assessed value off for 2025-2026 |

| Louisiana | Assessment freeze (special assessment level) | 65 | Yes | AGI cap ~$100K indexed; permanent once granted; Nov 2026 ballot may raise to $150K |

| Maine | Homestead exemption + senior-boosted credit | 65 | Credit: yes | Property Tax Fairness Credit max $2000 for 65+ (vs $1000 under 65) |

| Maryland | State homeowners credit (all ages) + county senior credits | 65 (county add-ons) | Yes | State circuit breaker has no age test; senior credits are county-option; annual application |

| Massachusetts | Exemption + deferral + circuit breaker | 65-70 | Yes | Clause 41C exemption (age 70 default; 65 local option); 41A deferral at 65 |

| Michigan | Homestead credit (all ages; senior-enhanced) | 65 (enhancement) | Yes | Max $1900 (2025); resources $71500 or less; value cap applies |

| Minnesota | Deferral (pay 3% of income; state pays rest) | 65 (spouse 62) | Yes | Income $96K or less; 5-yr ownership; interest capped at 5% |

| Mississippi | Exemption (first $7500 assessed value) | 65 | No | 2025-26 bills to raise to $12500 died in committee; $7500 stands |

| Missouri | County-option senior freeze + state credit | 62-65 | Credit: yes | HB594 raises credit to $1055 renters / $1550 owners from 2026 |

| Montana | Tiered homestead rates (all ages) + elderly credit | 62 (credit) | Credit: yes | Refundable credit up to $1150 (income under $45K); homestead application by Mar 1 |

| Nebraska | Sliding homestead exemption (up to 100%) | 65 | Yes | 2026: 100% relief up to $37K single / $43.4K married; phases out above |

| Nevada | No funded senior-specific program | – | – | STAR rebate was one-time (2015-16) and has concluded; general 3% cap applies |

| New Hampshire | Local elderly exemption (rises at 75 and 80) | 65/75/80 | Local | RSA 72:39-a; amounts + income/asset limits set by municipality; deferral available |

| New Jersey | Stay NJ + Senior Freeze + ANCHOR (one PAS-1 application) | 65 | Yes | Stay NJ 50% of bill up to $6500; first checks Feb 2026; quarterly |

| New Mexico | Valuation freeze | 65 | Yes | Income cap ~$41900 adjusted annually; apply with county assessor |

| New York | Senior exemption (local option; up to 65%) + Enhanced STAR | 65 | Yes | Dec 2025 law raised max from 50% to 65% where localities opt in |

| North Carolina | Elderly exclusion + circuit-breaker deferral | 65 | Yes | Exclusion: greater of $25K or 50% (income $38800); deferral caps tax at 4-5% of income ($58200) |

| North Dakota | Homestead credit (tiered) + Primary Residence Credit (all ages) | 65 | Yes | Up to $9000 taxable-value reduction at lowest tier; PRC up to $1600 for all owners |

| Ohio | Homestead exemption (indexed annually) | 65 | Yes | $29000 of market value for 2025 tax year payable 2026; income $40K MAGI |

| Oklahoma | Senior valuation freeze + additional homestead | 65 | Yes | Freeze income cap = HUD county median (varies); 65+ skip annual refiling on additional homestead |

| Oregon | Deferral (state pays; lien repays) | 62 | Yes | 2026 income limit $70K; 6% simple interest; 5-yr ownership |

| Pennsylvania | Property Tax/Rent Rebate | 65 (50 widowed) | Yes | Up to $1000 + supplements; 2025 income limit $48110; claims due June 30 |

| Rhode Island | Local exemptions + state credit (RI-1040H) | 65 | Yes | State credit max $700 (income $40730 or less); local programs vary |

| South Carolina | Exemption (first $50K fair market value; ALL property taxes) | 65 | No | Complete exemption on first $50K; 1-yr SC residency; school operating already exempt for all owner-occupants |

| South Dakota | Assessment freeze (65) + deferral (70) | 65 | Yes | Freeze income $56595 single / $66885 multi (2026); apply by April 1 |

| Tennessee | State-paid tax relief + local-option freezes | 65 | Yes | Reimburses tax on first $32700 of value (2025); income $37530 |

| Texas | $60K senior school exemption (atop $140K) + school tax ceiling + deferral | 65 | No | Raised from $10K by Nov 2025 vote effective tax year 2025 |

| Utah | Circuit-breaker credit + deferral (75+) | 66 | Yes | Credit up to $1312 + 20%-of-value credit; income under $42623; apply by Sept 1 |

| Vermont | Income-based property tax credit (all ages) | – | Yes | Max credit $8000 (income $115400 or less); no senior-specific exemption or statewide deferral |

| Virginia | Local-option exemptions and deferrals (vary widely) | 65 | Local | Va. Code 58.1-3210; each locality sets income/net-worth limits |

| Washington | Exemption + value freeze + deferral | 61 (deferral 60) | Yes | Lowest age threshold of any state; income limits vary by county |

| West Virginia | Exemption ($20K assessed value) | 65 | No | Apply by Dec 1; separate low-income senior tax credit exists |

| Wisconsin | General homestead credit only (no senior-specific) | – | Yes | Max $1168; income under $24680; owners and renters |

| Wyoming | 25% homestead (all owners; annual affidavit) + long-term 50% (65 + 25 yrs) + refund | 65 (long-term) | Refund: yes | Long-term exemption sunset REPEALED March 2026 (HB 45); 25% covers first $1M FMV; cannot stack the two |