Key Points

-

The annual COLA is set based on CPI-W data from the third quarter of each year.

-

The Senior Citizens League’s projected COLA for 2027 is 3.8%.

-

Social Security recipients have been losing purchasing power on their benefits.

Social Security benefits have been a lifesaver for many Americans over the years, with millions relying on them for their only source of retirement income. The program is far from perfect, but there’s one aspect I’m sure everyone can appreciate.

One of Social Security‘s long-standing features is the annual cost-of-living adjustment (COLA), which is intended to offset inflation. Retirees surely appreciate a boost to their benefits, but unfortunately, a larger COLA isn’t always good news because of the implications of the raise.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

How the annual COLA is calculated

The Social Security Administration determines the annual COLA by examining changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). It’s a three-step process:

- Average the CPI-W from the third quarter of the current year.

- Compare the current year’s average to the previous year’s average.

- Set the COLA as the percentage increase, rounded to the nearest tenth of a percent. (If the CPI-W average is less than the previous year, there’s no COLA.)

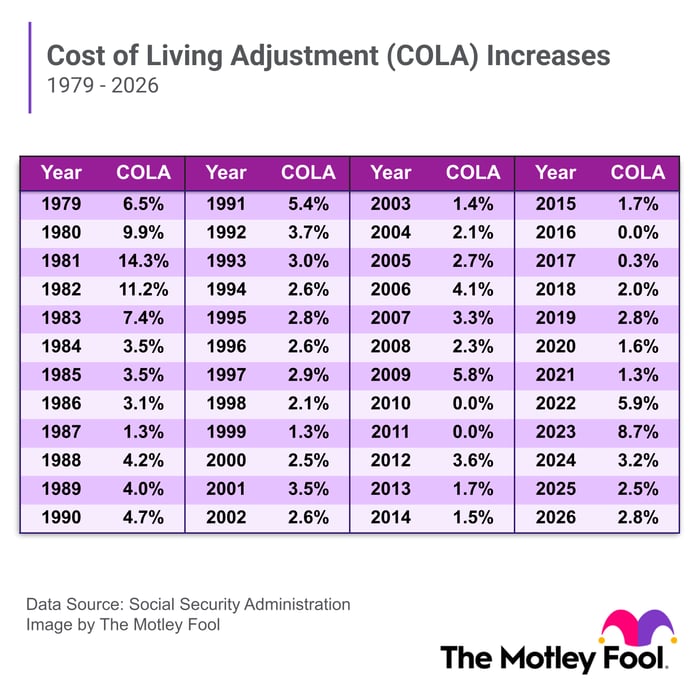

For example, the average in 2025 was 2.76% higher than in 2024, resulting in a 2.8% COLA for this year. Here is how past COLAs have shaped up:

Why a larger COLA isn’t always a good thing

Since the COLA is based on past inflation, it doesn’t help retirees address the rising costs they face today. A larger COLA means larger benefits in the upcoming year, but that doesn’t help when you go to the gas pump and spend $20 more per fill-up than you’re used to, or when the same groceries haul that would usually cost $150 now costs $200.

Take someone whose benefit was $2,000 in 2025, for instance. The 2.8% COLA would have boosted their benefits by $56, which could have easily been offset by rising expenses like gas, which increased by 7% in May.

Right now, The Senior Citizens League (TSCL) — a nonpartisan senior advocacy group — has its 2027 COLA estimate at 3.8%. That would be well above the average since COLAs became based on CPI-W data in 1977, and the fourth-highest in the past 20 years.

If the 3.8% estimate proves true, that would mean high inflation has persisted through most of this year, which, to say the least, isn’t ideal. Social Security won’t release the official COLA percentage until October, but at the current rate, it’s expected to be on the higher end.

Regardless of what the COLA is set at, the unfortunate reality is that retirees have consistently lost purchasing power with their benefits, and that trend doesn’t seem to be stopping anytime soon.

The $23,760 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income.

One easy trick could pay you as much as $23,760 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Join Stock Advisor to learn more about these strategies.

View the “Social Security secrets” »

The Motley Fool has a disclosure policy.