Key Points

-

There’s arguably no announcement more anticipated by Social Security recipients than the annual COLA reveal in October.

-

Social Security’s 2027 cost-of-living adjustment estimates are climbing as a result of Donald Trump’s actions in Iran.

-

However, a second consecutive year with a Trump bump won’t offset decades of disappointment for Social Security beneficiaries.

In March, the average retired worker brought home a Social Security benefit of $2,079.49. Though this annualizes to less than $25,000, this income is nevertheless vital to helping aged workers make ends meet.

For many of the 54.1 million retired workers currently receiving a Social Security payout, no annual announcement is of greater importance than the cost-of-living adjustment (COLA), which is revealed by the Social Security Administration (SSA) in October.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

For a second consecutive year, Social Security’s COLA is subject to an interesting quirk. Namely, actions taken by President Donald Trump will directly affect how much beneficiaries are bringing home each month in 2027.

President Trump delivering remarks. Image source: Official White House Photo by Joyce N. Boghosian, courtesy of the National Archives.

What, exactly, is Social Security’s COLA?

However, before digging into the details of how President Trump’s policies can impact Social Security payouts (again), it’s important to understand what Social Security’s cost-of-living adjustment is and how it’s calculated.

Imagine that you’re looking at a basket of hundreds of goods and services that seniors regularly purchase, and you notice that the aggregate cost of this basket has increased by 2% from the previous year. If Social Security benefits remained unchanged, recipients would lose buying power over time. Social Security’s COLA is the near-annual “raise” passed along to recipients that attempts to keep them on par with inflation (i.e., rising prices).

For the last 51 years, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) has been the program’s inflationary tether. The CPI-W has over 200 spending categories with unique percentage weightings. These percentages allow the CPI-W to be expressed as a single figure each month to quickly determine if prices are collectively rising (inflation) or falling (deflation).

Although the U.S. Bureau of Labor Statistics reports the CPI-W monthly, only trailing 12-month readings from the third quarter (July – September) are used in the cost-of-living adjustment calculation. If the average third-quarter CPI-W this year is higher than the same period in 2025, beneficiaries are due a raise.

The amount that benefits rise is determined by the year-over-year percentage increase in average third-quarter CPI-W readings, rounded to the nearest tenth of a percent.

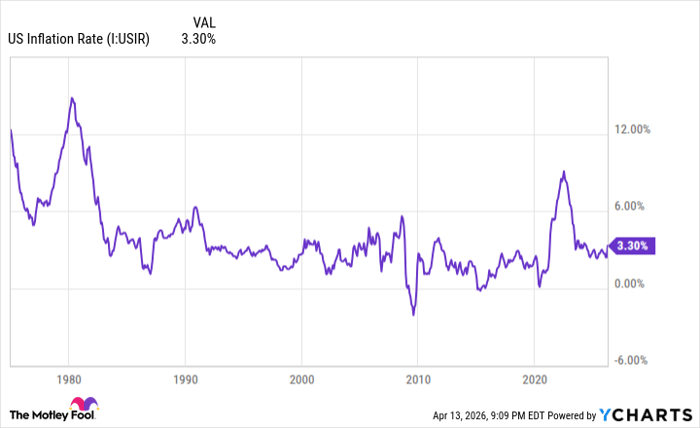

A higher inflation rate has led to larger Social Security COLAs in recent years. US Inflation Rate data by YCharts.

Social Security payouts are in line for another “Trump bump”

Making history has been something of the norm for America’s foremost retirement program over the last year. In May 2025, the average retired-worker benefit surpassed $2,000 for the first time since Social Security’s inception.

Additionally, the 2.8% cost-of-living adjustment passed along this year marks the fifth consecutive year that benefits have risen by at least 2.5%. The last time that happened was three decades ago.

But what’s noteworthy about the 2.8% raise beneficiaries received in 2026 is that it was aided by a “Trump bump.” Donald Trump’s tariff and trade policy increased prices on select imported goods and domestic manufacturers, leading to sticky goods sector inflation. In other words, Trump’s tariffs directly led to higher nominal Social Security checks for recipients this year.

Based on early estimates for Social Security’s 2027 COLA, beneficiaries are likely to see a Trump bump, yet again — but this has nothing to do with tariffs.

At President Trump’s command, U.S. military forces, along with Israel, commenced attacks on Iran beginning Feb. 28. Shortly after this conflict began, Iran closed the Strait of Hormuz to virtually all oil shipping traffic. The Iran war has precipitated the largest energy supply disruption in modern history.

Over the last seven weeks, crude oil prices have soared, and fuel prices have followed suit. Consumers are getting pinched at the pump as gas prices soar, while businesses are paying more for transportation and/or production costs. This energy price shock is beginning to show up in the monthly U.S. inflation report, and it’s having a tangible impact on 2027 COLA forecasts.

According to nonpartisan senior advocacy group The Senior Citizens League (TSCL), the 2027 COLA is expected to be 2.8%. Meanwhile, independent Social Security and Medicare policy analyst Mary Johnson anticipates the 2027 raise will be 3.2% — nearly double her previous forecast of 1.7% before the Iran war began.

If we were to use the middle ground between these two estimates (3%) as the base COLA case for 2027, the average retired-worker beneficiary would see their monthly payout rise by more than $62.

In comparison, the average worker with disabilities and the average survivor beneficiary would see their monthly checks each climb by approximately $49 in 2027.

Image source: Getty Images.

Social Security’s Trump bump won’t offset decades of disappointment

While Trump’s actions are expected to have a notable impact on Social Security benefits for a second consecutive year, a potentially beefier raise for 2027 won’t offset what’s been decades of disappointment for retirees.

Although the CPI-W is designed to closely mirror the effects of inflation on program recipients, it hasn’t done a good job of this.

The problem is evident in its full name: the Consumer Price Index for Urban Wage Earners and Clerical Workers. “Urban wage earners and clerical workers” are typically working-age individuals who aren’t currently receiving a retired-worker benefit. Even though 87% of Social Security’s beneficiaries as of December 2024 were 62 or older, the program’s inflationary index is tracking the spending habits of predominantly working-age Americans — and that’s a problem.

Working-age individuals and retirees spend their money differently, with seniors apportioning a higher percentage of their budgets to shelter and medical care services. The CPI-W simply isn’t accounting for the added importance of these expense categories for retirees.

To make matters worse, Social Security has been without its silver lining for three consecutive years. This is to say that Medicare’s Part B premium — the outpatient services segment of traditional Medicare — has been climbing at a rapid pace, leading to partial or even full offsets of annual COLAs.

According to TSCL, the buying power of Social Security income has plummeted by 20% from 2010 to 2024. A modest Trump bump in back-to-back years isn’t going to alter decades of weakening purchasing power.

The $23,760 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income.

One easy trick could pay you as much as $23,760 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Join Stock Advisor to learn more about these strategies.

The Motley Fool has a disclosure policy.

53 Comments

Does Motley Fool now hire people who can’t do 2nd grade math? The middle ground between 1.7% and 3.2% is not 3%.

(1.7 + 3.2)/2 =2.45%

You’ve got the wrong numbers in your equation. It should be the Senior Citizens League’s projection of 2.8% added to 3.2%, policy analyst Mary Johnson’s current forecast, not 1.7%, her previous forecast. 2.8% plus 3.2% equals 6%, divided by 2 equals 3%. The number given in the article is correct.

Let’s have dumb ass congress and the president live on ssi for a year and see what happens

Social security was never intended to be the sole form of income for people. It’s a supplemental income only. Didn’t your daddy teach you that old statement “Save for a rainy day”?

Social security was set up to help the windows of WW2.

Workers at one time got retirement from the Company s they had worked for.

sure they can bump s.s. but every time it increases Medicare goes up more, so we still lose in the end!

President Trump does not take a salary and i believe he also hasn’t taken any S.S. checks even at 80 yrs old. He earned, invested and saved and doesn’t need to rely 9n that income.

I wouldn’t give you a nickle for anyone in the house or senate.

That’s because he’s grifting off our treasury…

PROOVE IT!!!

Another lie you have believed.

What ever they give for a COLA increase will be conveniently taken from MEDICARE for money through scandalous insurance companies greed. It ALWAYS works. That way. 2.percent increase in S.S. and a 2 percent increase in MEDICARE. How convenient 🙄 😒 😡👿

That’s exactly what happens……..

AGREE, THIS year w/ the “bump” i came away w/ 21.00.. Medicare and advantage took most of the 71.00 increase..THEY try to make it like a real increase.. I laugh in their general direction..

Dear Luke, The fact that you use a Monte Python phrase distinguishes you as a man of great learning and sophistication. I applaud your ecclectic intellect.

I laughed when I saw this article, because I was thinking the exact same thing you posted.

As soon as we get the COLA increase, Medicare takes it by raising premiums. What a joke.

“Additionally, the 2.8% cost-of-living adjustment passed along this year marks the fifth consecutive year that benefits have risen by at least 2.5%. The last time that happened was three decades ago.” 2025’s increase occurred under Trump; all the rest were under Biden, so many thanks to President Biden for helping seniors keep up, at least a little. As far as an increase of 3.2%, as with everything else that may have a positive impact to America under the Trump regime, I’ll believe it when I see it.

Biden created 12%+ actual inflation which increased retiree cost of living. He and democrats raised taxes, the cost of enery, the cost of food, the cost of housing, the cost of insurance, fuel prices, the cost of medical care, etc. Then he opened the borders and made taxpayers pay for all the illegals benefits, food, medical care, and hpusing, and funded NGO’s. He did no one any good except for his dem donors and CEO’s of large corporations that ran green energy corporations. Want to rethink your praise for President autopen?

Trump said he was going to stop taxing social security benefits, what happened to that bump?

Did he mean if social security was your only income there would be no tax…..

The same thing that happened to “No tax on overtime”

It’s all a shell game hoping to distract you.

The “No tax on overtime” ended up being only no tax on the .5 part of the 1.5 overtime rate, not not tax on any time worked after 40 hours per week.

But don’t get too excited, there is also a cap on the amount you can claim when you file your taxes

Geez guys, give him some credit, he’s doing a LOT more than anyone before! You can’t fix everything overnight, especially with the crazed leftists foaming at the mouth doing everything they can to stop him! He actually did from what my CPA said, but was ‘overuled’ and we only received a portion of the relief he wanted to give us. I haven’t researched the specifics, sorry…

He actually did from what my CPA said, but was ‘overuled’ and we only received a portion of the relief he wanted to give us. I haven’t researched the specifics, sorry…

Why don’t you just give all retires 1000.00 dollar permanent raise? We should be receiving more anyway. Congress stole our money. Take it out of their money. They are all millionaires.

WHEN?

If Social Security gets an increase I’ll pay even more taxes in ’28 than I did this year. NO THANKS

Why did you pay more last year? We all got a big deduction (thanks to Trump’s OBBB) and I paid $1,500 LESS in income taxes last year!

Yes, we were stunned to get $2400 back. Absolutely stunned. Thank you, President Trump!

assuming yo are taxed at a 20% rate (About average) a tax increase will let you keep 80% of your increase. Said another way, paying 20% more taxes, but getting 80% more in reality seem like a pretty good deal to me!

I wonder how the raise they give seniors is compares to the raises congress is always giving themselves.

Simple answer: American politicians are only interested in making sure they remain wealthy–they couldn’t care less about the average American and what we struggle with on a daily basis because of their (the politicians) illegal activities.

Congress hasn’t received a pay raise since 2009.

There is no way I believe that!!

While I just fact-checked you and see that you are correct, I don’t care that they haven’t received a raise since 2009. Have you seen how much they make? AND they get that for the rest of their lives once they leave the House and Senate.

I thought they just gave themselves $30,000 each.

Yes, in 2023 they changed the rules so they can now reimburse themselves as much as $30,000 to cover “living expenses” in D.C. Not technically a pay raise, but amounts to the same thing (and may be better, if the money isn’t taxed as income).

You are talking about a base salary. Add a lot more for committee chair positions, free food, free healthcare, and a host of other perks…. If they are underpaid, why do they keep running for re-election?

As usual, Medicare premium will take majority of it…. besides fuel, food that are not listed now in the cpi What a joke…

Retired into poverty, barely making my property taxes to keep the home i worked my whole life for. I get less than 100 in ebt that’ll I’ll lose half of, medicare gets their share before I even get my check. Cola’s are a shell game anything “extra” goes back to the government anyway, What a joke.

Never bothering to open a retire.ly post again and the Motley Fool appears to be more fool than motley. Pushing the angle of a “Trump bump” as a good thing is ridiculous for asinine policies that resulted in wild inflation and the process for increases is what is trying to offer us some protection FROM morons like Trump. GOP policies have been horrible for Social Security and its recipients. Privatization is their long goal.

My condolences that you would even consider that the leftists in charge EVER made your life better!! Good luck in THAT thinking!!

Sounds like you have a terminal case of TDS.

Congress uses the social security issue as a political football, when they address it at all. Pres Trump has proven that he does care about this issue, but it is Congress who is the stumbling block to any and all corrective action. The Congress must develop and present legislation to the President. The President can’t unilaterally “fix” the problems with SS, MediCare, etc It is the Congress who must do and deliver – and they’ve proven that they care more about destroying the other party than really working for American citizens.

Clearly our government believes we are all idiots. It is simple math and nothing they say will change it. I remember it being said ” what one hand givith the other takes away. Very true of the government of the United States of America. Somewhere along the road the people have lost ALL the Power that we are supposed to have. The politicians live off the people like the parasites they are. Not sure how we can fix this mess or even if there is a way to fix it.

The problem is, Social Insecurity will go after recipients, taking their money claiming they received over pay. I know. They did it to us.

They did this to me as well, they took what was the exact amount of my backpay. They steal our money because they can and we have little remedy to fight them.

SS DOGE Department is necessary to make our very own government return all money they extracted from SS trust found last 25 years. SS become Piggy Bank for politicians. Make them return money where belong.

It amazes me that so many people think Trump is giving more the the SS beneficiaries. They literally don’t understand how COLA works.

These COLAs are a disgrace, 2.8%, 3.2%. In the meantime, 112 million renters in America are routinely seeing 10-15% increases in rent (your most expensive constantly ongoing expense). And over the past 4 years, rents have skyrocketed 100-200%. What was $750/mo 4 years ago, is now $2500/ mo. Cost of homes are way up too. These COLAs are an insult.

Social Security….. kind of like the American Dream. Both are a nightmare today.

Hello, just testing since my last post failed.

Trump refund social security. Politicians stealing all of our money over the years. Our government wasting billions of dollars. REFUND SOCIAL SECURITY!! NOW!! I know you can get the money.

so-so cola raises. Insurance cost eats up raise. Last time, I ended up with $27 dollar increase a month. Yahoo for cola . If you make over $1000 a month, forget about all those so-called extra benefit’s. I want refunds for social security.